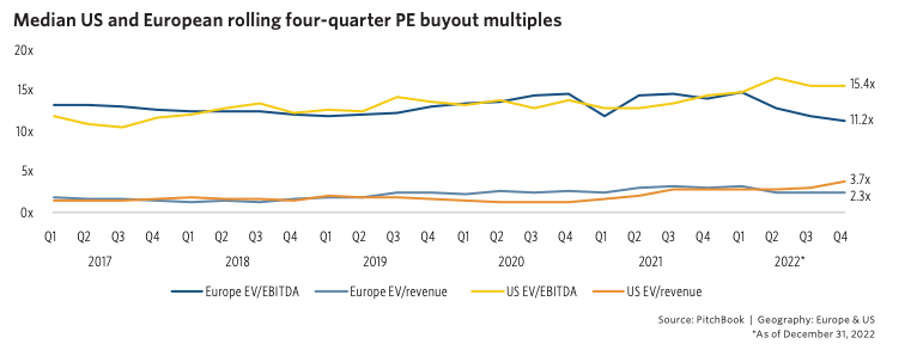

In 2022, purchase price multiples diverged between Europe and the US. Europe's rolling four-quarter EV/EBITDA multiples declined from a Q1 peak of 14.6x to 11.2x in Q4. In contrast, the US experienced higher EV/EBITDA multiples, peaking in Q2 2022, with a slight plateau in Q3 and Q4. Similar trends were observed in EV/revenue multiples.

This is particularly surprising since both regions tracked each other for the best part of the last 15 years.

How can we explain this divergence?

High competition, high multiples

The US private equity (PE) market is larger, more liquid, and more competitive than Europe's, accounting for 60% of the world's PE assets under management (AUM) and being nearly three times bigger than Europe. Higher competition in each market increases the likelihood of obtaining higher multiples in dealmaking. During due diligence, sponsors conduct relative valuations using multiples from similar transactions within the sector and current multiples from public companies.

Dominant sectors dictate multiples.

The US dominates the tech sector more than Europe, resulting in higher EV/revenue and EV/EBITDA multiples. The US's tech-heavy industry, particularly enterprise software and IT services, has driven higher multiples due to strong demand for businesses with recurring revenue models, high growth, and high margins. These businesses showed resilience during the COVID-19 pandemic. However, 2022 saw a market correction, particularly in tech, forcing companies to focus on fundamentals and operational efficiencies. Despite challenges in the next 12-18 months, tech will remain a dominant sector and driver of buyout multiples, but median multiples may decrease from elevated levels caused by a 12-year bull market.

Key takeaways

- In 2022, purchase price multiples for LBOs diverged between the US and Europe. European PE buyout multiples declined, while US multiples increased due to higher competition, larger investor pools, more stimulus, and a dominant tech sector. This divergence may not persist medium-term, with US multiples expected to contract similarly to Europe's. However, the US should maintain a small premium moving forward.

- Public multiples no longer command a premium over private multiples, as the gap between them has converged. Private equity is expected to grow as an asset class, becoming more accessible to various industry players. Consequently, private equity will increasingly dictate buyout multiple levels, leading to the continued disappearance of the traditional premium associated with public markets.

- IT and healthcare drive median buyout multiples higher. We expect these two sectors will continue fetching higher multiples than other sectors in the medium to-long-term, although the median multiple in these sectors may correct in the short term due to the shift in monetary policy and credit conditions. Credit spreads are widening, borrowing costs are rising, and leverage is falling for buyout sponsors, all consequences of higher interest rates, which negatively impact buyout multiples.

- EBITDA growth is becoming the key driver of outperformance as macroeconomic factors shift PE strategies away from multiple expansion and leverage. Manager selection gains importance for LPs, who must choose managers capable of adding value through fundamental growth instead of just multiples expansion. Track records become crucial, and first-time managers may struggle.